The Global EV Dilemma: Risks of Over-Reliance on China

Reading time: 10 min

Last Updated: Mar 11, 2025

-

![Shipra Sanganeria]()

-

![Felipe Allende]()

Fact-Checked by Felipe Allende Cybersecurity & Tech Writer

The global shift to electric vehicles (EVs) is accelerating, driven by environmental concerns, government policies, and rapid technological advancements. However, this transition comes with a major challenge: China’s dominance over the EV and battery supply chain.

China’s economic policies, supply chain dominance, and technological advancements have accelerated global adoption of its EVs, but have also created economic and geopolitical risks for nations heavily reliant on Chinese production. The key question is: Can the US, Europe, and other markets develop self-sufficient EV supply chains to reduce their dependency on China?

Aligned with WizCase’s commitment to data-driven global insights, this research examines China’s rise as the EV leader, the risks of over-reliance on a single nation, and the steps other economies are taking to counterbalance its dominance.

The article also explores advancements in battery technology, trade policies, and the future landscape of global EV manufacturing.

China’s EV Dominance: Why It Leads and Why It’s a Risk

China dominates global electric vehicle (EV) production, controlling nearly 70% of manufacturing and 77% of battery production. This dominance can be attributed to decades of government-backed investments in infrastructure, research and development (R&D), and industrial subsidies.

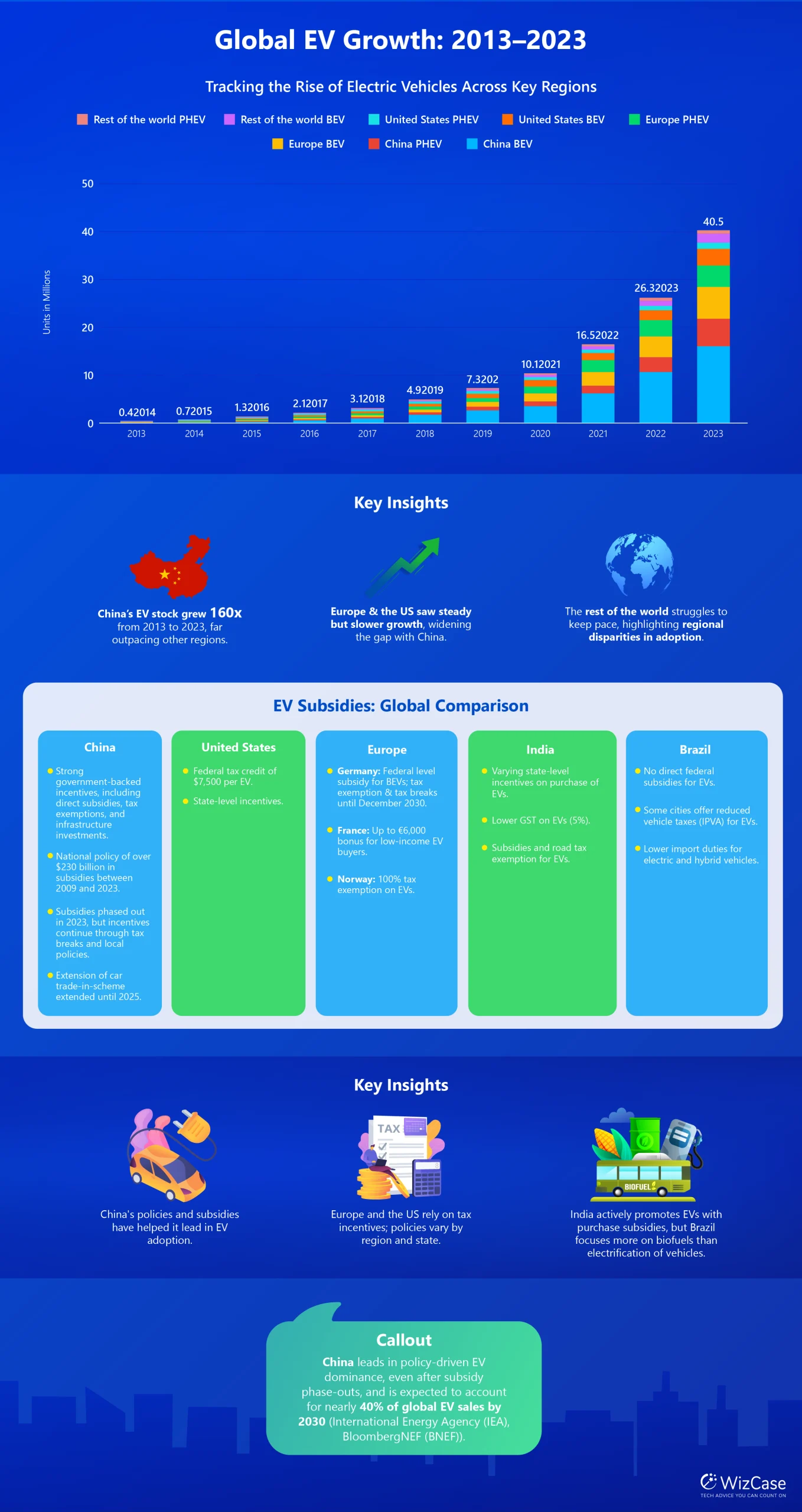

Between 2017 and 2023, China’s EV exports surged 13,300% to $42 billion, when it produced nearly 70% of the world’s EVs. According to the International Energy Agency (IEA), China’s 2023 EV stock included 16.1 million battery electric vehicles (BEVs) and 5.8 million plug-in hybrid electric vehicles (PHEVs).

It far surpassed European (6.7M BEVs, 4.5M PHEVs) and US (6.3M BEVs, 1.3M PHEVs) car stocks. The rest of the world combined had just 1.9 million BEVs and 0.7 million PHEVs. The graphic below illustrates China’s rising dominance in EV stock over the past decade.

China’s long-term strategic policies have fueled both EV production and domestic adoption. Additionally, the government’s open approach to EV manufacturing, allowing foreign companies like Tesla to establish operations, has intensified competition and innovation within the industry.

China’s EV Battery Supremacy

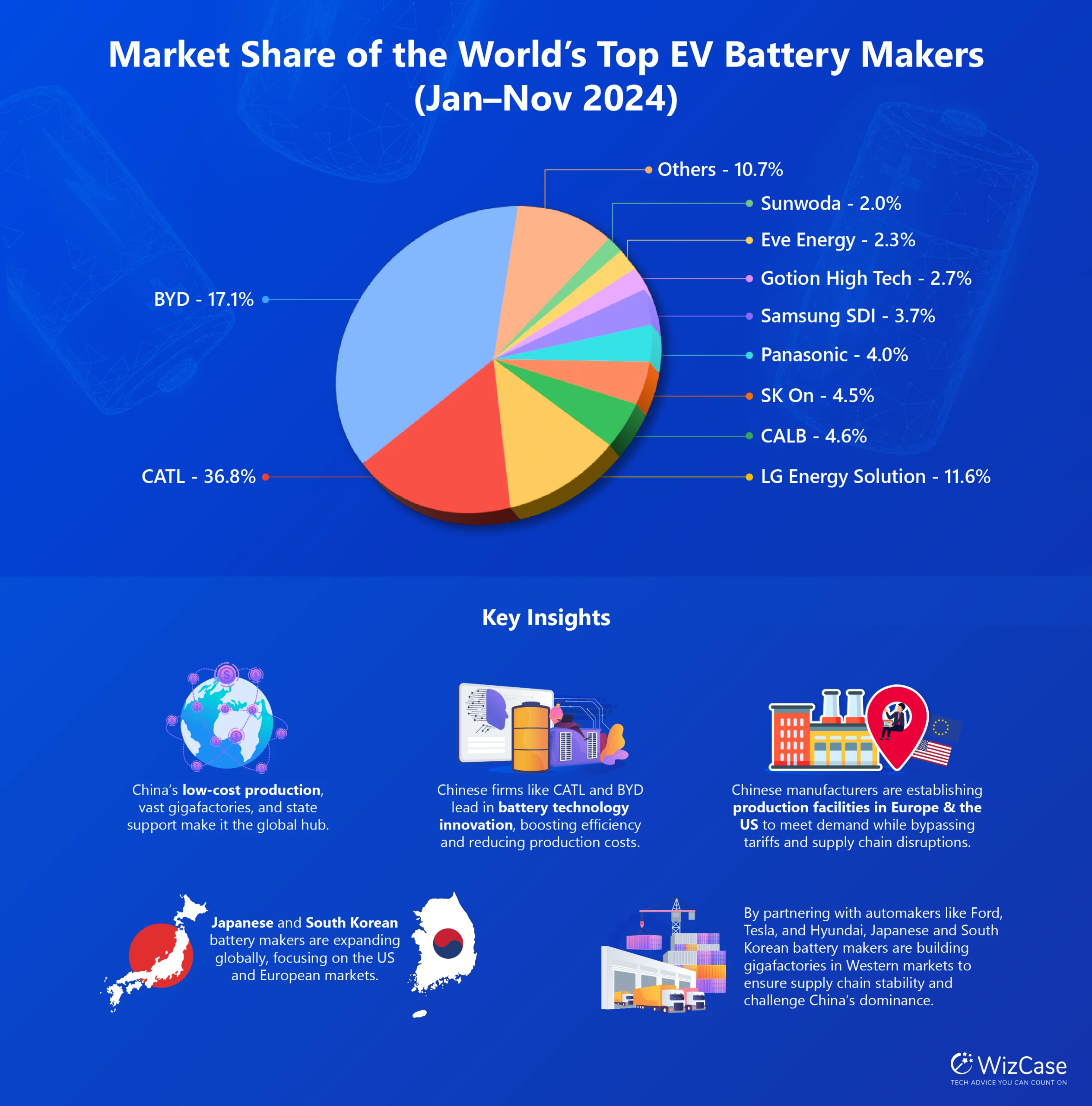

Beyond policy, China’s dominance in battery technology has been a major advantage. As the world’s largest EV battery producer, Chinese manufacturers like CATL and BYD alone account for over 50% of the global EV battery market.

Chinese companies control over 65% of the global EV battery market, with a single company, CATL, commanding over 30% of the market share. This illustrates just how far ahead Chinese manufacturers are compared to their global counterparts, and their ability to maintain control over pricing, supply chains, and technological innovation.

According to SNE Research, South Korean and Japanese manufacturers such as LG Energy Solution (11.6%), SK On (4.5%), and Panasonic (4%) are struggling to catch up.

To reduce their reliance on China, these companies are expanding their production capabilities in the US and Europe and also forming key partnerships with automakers like GM, Hyundai, and Tesla. However, their efforts to secure supply chains and establish themselves as serious competitors still lag behind China’s strong market position.

China’s Smart EV Infrastructure Investment

China’s heavy investment in EV infrastructure has positioned it as the global leader in electric vehicle adoption. Its extensive network of both fast and slow chargers outpaces the combined total of all other regions, including both the US and Europe, reinforcing China’s dominance in the sector.

By 2023, China had 1.5 million slow chargers and 1.2 million fast chargers, surpassing the global total of 0.9 million and 0.18 million, respectively.

This gap persisted in 2024, with China reaching 3.4 million public charging points (AC & DC) by July 31, far ahead of the US (0.2 million) and Europe (1.02 million). This widespread network reduces range anxiety and supports daily EV use, accelerating EV adoption.

Compared to other regions and countries, China’s strategic urban planning has ensured charger availability in residential, highways, and commercial areas. Additional incentives, such as lower charging costs and reduced registration fees, has further boosted EV adoption.

As the world plays catch-up, the global future of EV adoption hinges on how quickly other countries can expand their charging infrastructure to reduce dependence on China.

Global Strategies: Reducing Reliance on China’s EV Industry

As China solidifies its dominance, Western nations and other economies are working toward building independent supply chains through tariffs, state-backed investments, and battery innovation. Nevertheless, breaking China’s grip on the EV industry remains one of the biggest economic challenges of the decade.

Below is an overview of strategic steps taken by key economies in 2024, to reduce their reliance on Chinese-manufactured EVs and batteries:

| United States | Europe | India | Other Countries |

|---|---|---|---|

|

|

|

|

Despite the strategic measures being taken, scaling up the production of electric vehicles (EVs) and their components remains a significant challenge that will require years to overcome.

Key hurdles include bridging technological and production gaps, securing the raw materials such as lithium and cobalt (needed for batteries), and building of critical infrastructure like gigafactories and specialized facilities.

All of this demands significant amounts of capital and time investment. Furthermore, shifting trade policies, tariffs, and global political dynamics add complexity to the process, slowing down efforts to boost production.

Even though countries are working to lessen their dependence on China for EV production, scaling up domestic manufacturing is a multifaceted challenge that will require sustained long-term investment.

The Battery Tech Battle: Can Innovation Challenge China?

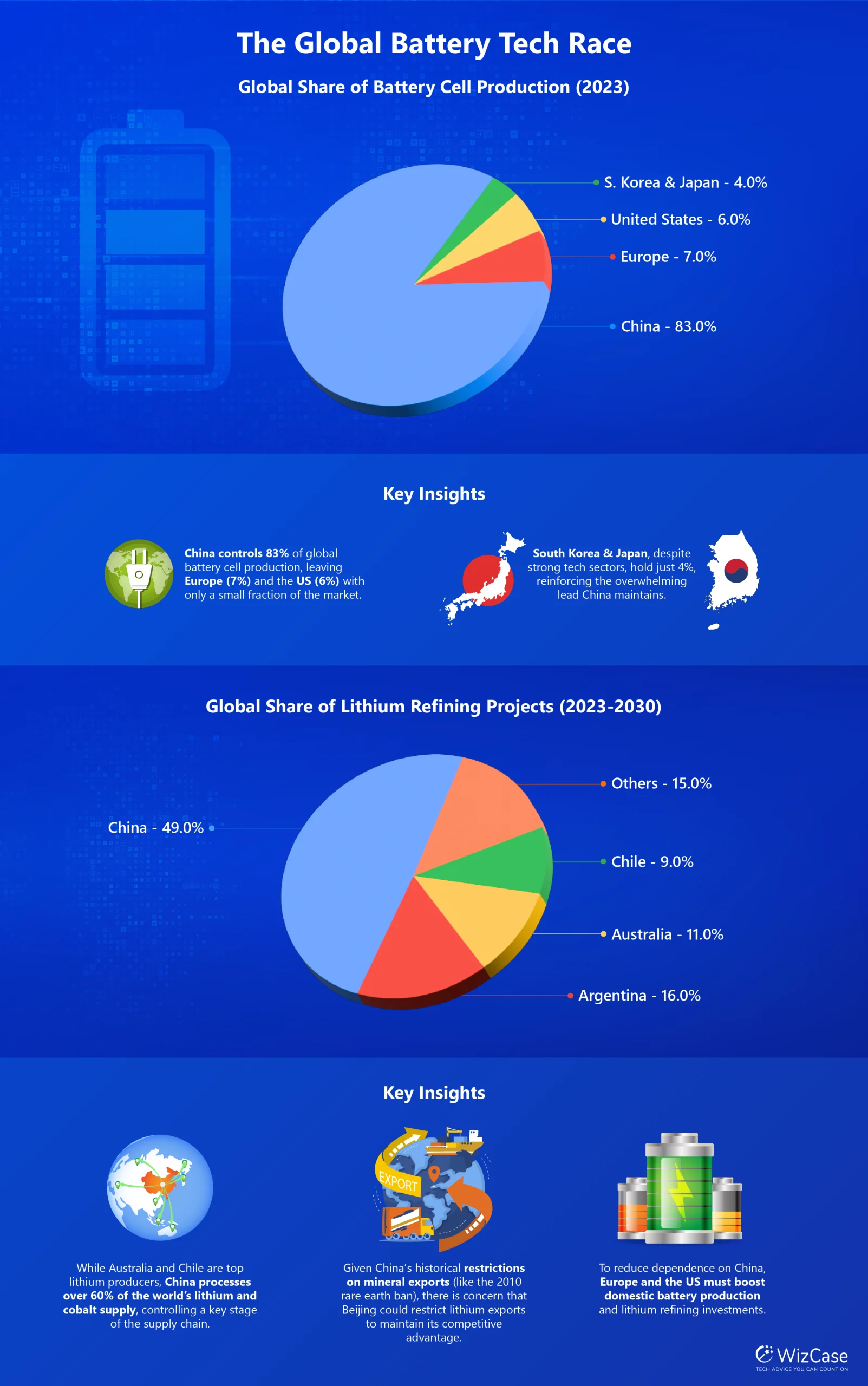

In 2023, China remained the dominant force in the battery supply chain, processing over 60% of the global lithium and cobalt supply and accounting for nearly 83% of global battery cell production capacity. In contrast, during the same period, Europe, the US, and South Korea each held 10% or less of the supply chain for key battery metals and cells (IEA). This continued dominance has helped China control pricing, supply security, and innovation trends across the industry.

As illustrated above, China leads in processing the most critical minerals needed for EV battery production. Looking ahead IEA predicts that China will account for over 90% of battery-grade graphite and 77% of refined rare earths by 2030.

This control over the supply chain raises the risk of potential export restrictions, similar to the 2010 rare earth export ban. Recent actions, such as Jiangsu Jiuwu Hi-Tech halting lithium processing technology exports, signal that China could use its control as a strategic tool amid rising trade tensions.

We are monitoring updates for 2024 data and will revise these figures accordingly.

Alternative Battery Technologies & Their Potential Impact

Sodium-Ion Batteries: A Game-Changer?

Sodium-ion batteries are emerging as a cost-effective alternative to lithium-ion batteries. They’re potentially 20-30% cheaper and eliminate the need for both lithium and cobalt.

However, China holds over 90% of sodium-ion battery manufacturing, with CATL leading innovation. Depending on global adoption, this technology could either challenge China’s dominance on lithium-based batteries or further solidify its leading position in the battery supply chain.

Solid-State Batteries: A Long-Term Bet

Solid-state batteries promise longer ranges, faster charging, and extended lifespans. Companies like Toyota and QuantumScape are investing heavily in development, but mass production remains at least five years away, making it a longer-term solution to diversifying battery technology.

As demand for electric vehicles grows due to international climate goals and regulations, reducing battery costs becomes increasingly crucial for competitiveness. China’s innovation in battery technology has driven lithium-ion costs down by nearly 90% since 2010 (BloombergNEF), with companies like CATL and BYD leading advancements in LFP batteries.

While solid-state batteries hold promise, their high production costs and long production timeline mean China’s dominance in lithium-based batteries remains strong for now, though alternative battery technologies like sodium-ion offer potential in the future.

What Happens Next? The Future of Global EV Manufacturing

The future of global electric vehicle (EV) manufacturing is poised for dramatic shifts, driven by geopolitical tensions, trade policies, and emerging manufacturing hubs.

India and South Korea as Alternative Hubs

As global manufacturers aim to reduce their dependence on China, India and South Korea are emerging as potential EV manufacturing hubs.

India’s growing infrastructure, competitive labor costs, and government incentives are making it an attractive location for EV production. However, the country still faces significant challenges, including infrastructure gaps and heavy dependence on Chinese imports for key materials.

South Korea, with its established battery manufacturing base (like LG Energy Solutions, SK Innovation, and Samsung SDI), is already a key player in the global EV supply chain and is expanding its presence in markets like North America and Europe. Nevertheless, it remains reliant on Chinese rare minerals and technology, limiting its raw material independence.

Intensifying trade wars, shifting policies, and supply chain diversification efforts are reshaping global EV manufacturing. With China controlling critical mineral exports, risks of export restrictions could disrupt the supply chain.

As new nations rise as alternative EV hubs, and key markets like the US and Europe aim to regain dominance, these shifts will define the future of global EV production.

Methodology

This research examines China’s dominance in the global electric vehicle (EV) market using multiple data sources, including industry reports and government policy analyses.

Initially, we reviewed global EV market reports to understand the overall growth in electric vehicle sales, with a particular focus on China and the factors driving its success in the sector.

We then compared China’s approach with that of its competitors, such as the US and Europe, to identify the strategies and policies that have shaped the leadership of these regions in the EV space.

Collectively, these insights provide a thorough understanding of the dynamics behind China’s leadership and the evolving global landscape of EV adoption.

Discussion

In conclusion, the shift to electric vehicles (EVs) is being accelerated by environmental concerns, government policies, and technological advancements. However, China’s dominance in EV and battery production presents significant economic and geopolitical risks for other regions.

While countries like India and South Korea are positioning themselves as alternative EV manufacturing hubs, challenges such as infrastructure gaps and reliance on Chinese raw materials remain.

As global trade policies and supply chain diversification efforts accelerate, these factors will shape the future of global EV production, with emerging and key markets working to reduce dependence on China’s strong foothold in the industry.

Leave a Comment

Cancel